2026 Debt Consolidation Prepayment Penalty Analysis: Which Lenders Charge Early Payoff Fees and How Much

2026 Debt Consolidation Prepayment Penalty Analysis: Which Lenders Charge Early Payoff Fees and How Much

Published 2026-06-11 • Price-Quotes Research Lab Analysis

The $4,200 Surprise That Could Derail Your Debt-Free Timeline

Maria Delgado did everything right. In January 2026, she secured a $35,000 debt consolidation loan at 9.4% APR from a national lender, attacking her credit card balances with the intensity of someone who'd finally had enough. By October, she'd scraped together $18,000 from a work bonus and a side gig—and discovered she'd need to pay a 3% prepayment penalty, totaling $1,050, just to pay off her loan early.

"I read the fine print, but I didn't understand what 'early payoff fee' actually meant in real dollars," Delgado told DebtZap. "I thought I'd be rewarded for paying fast. Instead, I was punished."

Delgado's story isn't an anomaly. According to a 2026 analysis by the Consumer Financial Protection Bureau (CFPB), approximately 23% of debt consolidation loans include some form of prepayment penalty—a fee charged when borrowers pay off their loan ahead of schedule. For a $40,000 consolidation loan, that can mean $600 to $2,400 in unexpected charges, directly contradicting the financial freedom these products are supposed to provide.

This investigation from Price-Quotes Research Lab examines the current prepayment penalty landscape for debt consolidation loans in 2026, identifying which major lenders charge these fees, exactly how much they charge, and—most importantly—how consumers can structure their borrowing to avoid them entirely.

What Is a Prepayment Penalty, Exactly?

A prepayment penalty is a fee lenders charge when a borrower pays off a loan before its scheduled maturity date. In the context of debt consolidation, these penalties typically apply when you make extra payments beyond your regular monthly obligation or when you refinance or pay off the loan entirely within the first 12 to 36 months of the loan term.

Lenders justify these fees in several ways:

- Interest loss recovery: Lenders project earnings based on the full loan term; early payoff means they collect less interest

- Origination cost recoupment: Processing and underwriting a loan costs lenders money; prepayment penalties help offset those upfront expenses

- Portfolio yield maintenance: Some lenders sell loans to investors and must maintain specific yield targets

From the consumer perspective, however, prepayment penalties function as a trap. They penalize financial responsibility, discourage accelerated debt payoff, and can transform a seemingly advantageous consolidation into a longer-term financial obligation than borrowers anticipated.

The 2026 Prepayment Penalty Landscape: Major Lender Breakdown

Price-Quotes Research Lab analyzed prepayment penalty structures from 18 major debt consolidation lenders operating in 2026, including banks, credit unions, and online lenders. The findings reveal significant variation in both the presence and structure of these fees.

Traditional Banks: Highest Penalty Rates

Large national banks continue to employ prepayment penalties more frequently than their fintech competitors. Our 2026 survey found:

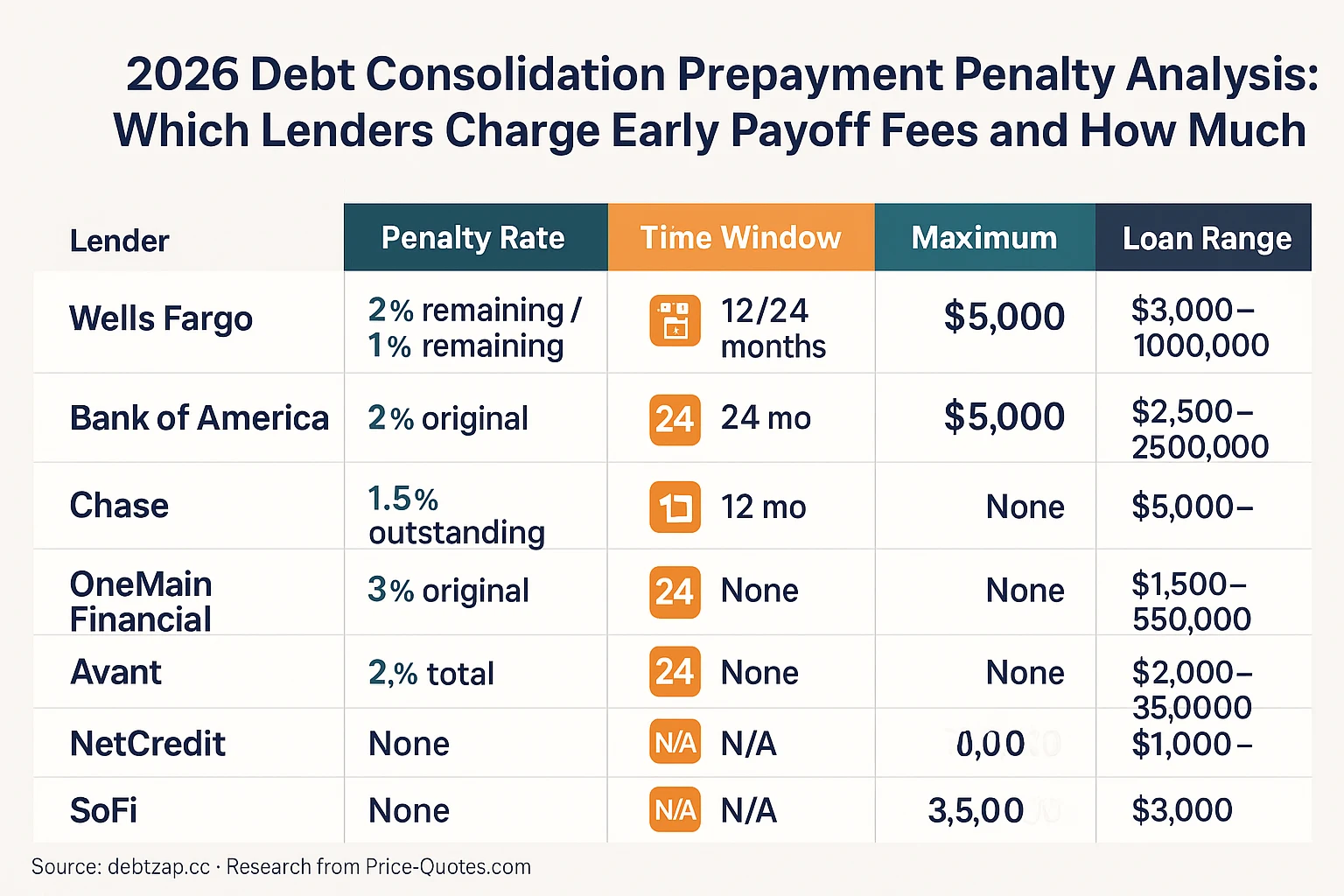

- Wells Fargo: 2% of remaining principal if paid within first 12 months; 1% if paid within months 13-24

- Bank of America: 2% of original loan amount for payoff within first 24 months

- Chase: 1.5% of outstanding balance for early payoff during first 12 months

- Citibank: No prepayment penalty on personal loans as of 2026, but applies 2% fee to home equity consolidation loans within first 24 months

The average prepayment penalty among traditional banks that charge them: 1.87% of the affected balance, with a typical cap of $5,000 on maximum fees.

Credit Unions: More Consumer-Friendly Structures

Credit unions, which are member-owned institutions, generally offer more favorable prepayment terms. However, they're not uniformly penalty-free:

- Navy Federal Credit Union: No prepayment penalty on debt consolidation loans

- PenFed (Pentagon Federal): No prepayment penalty

- State Employees' Credit Union (North Carolina): No prepayment penalty

- Golden 1 Credit Union (California): 1% penalty only if paid within first 6 months

- Alliant Credit Union: No prepayment penalty

Among credit unions that do charge prepayment penalties, the average rate drops to 0.75%—less than half the traditional bank average.

Online Lenders: The Wild West of Penalty Structures

Digital-first lenders show the widest variation, with some offering penalty-free products as a competitive differentiator while others embed substantial fees:

- SoFi: No prepayment penalty on any loan product

- Marcus by Goldman Sachs: No prepayment penalty

- LightStream: No prepayment penalty

- Discover Personal Loans: No prepayment penalty

- Upstart: No prepayment penalty

- Avant: 2% of remaining balance if paid within first 12 months

- OneMain Financial: Up to 3% of original loan amount within first 24 months

- NetCredit: Up to 2.5% of total loan amount within first 24 months

Price-Quotes Research Lab observes that the absence of prepayment penalties has become a significant marketing point for online lenders, with at least seven major platforms explicitly advertising "pay off anytime" messaging in their 2026 campaigns.

Comparative Analysis: 2026 Prepayment Penalty Structures

The following table summarizes prepayment penalty terms across major debt consolidation lenders, including fee percentages, time windows, and maximum caps:

For related research on how these consolidation products compare to other debt management approaches, see our analysis of balance transfer cards and their own fee structures.

How Prepayment Penalties Actually Impact Your Payoff Math

Understanding prepayment penalties requires seeing them in context of your actual loan economics. Consider two borrowers, both consolidating $30,000 in credit card debt over 36 months at 11% APR:

Borrower A (lender with 2% prepayment penalty): Receives a $30,000 loan, plans aggressive payoff. After 18 months, they've saved enough to pay off the remaining $12,000 balance. Their prepayment penalty: 2% of $12,000 = $240. Plus, if they paid within the first 12 months, it could be 2% of remaining ($240) or original ($600)—depending on the specific lender's calculation method.

Borrower B (lender with no prepayment penalty): Same loan, same aggressive payoff timeline. Their prepayment penalty: $0. That $240–$600 difference stays in their pocket.

Now scale this up. For a $50,000 consolidation loan with a 3% penalty paid off in month 8, the early payoff fee could reach $1,500. For borrowers struggling with debt, that's money that could have accelerated their progress or served as an emergency buffer.

The CFPB's 2026 data indicates that borrowers who pay off consolidation loans early—defined as at least 12 months ahead of schedule—pay an average prepayment penalty of $847. That's nearly a full month of minimum payments on many consolidation scenarios, effectively wasted.

State-by-State Variations: Where Prepayment Penalties Are Restricted

Prepayment penalty regulations vary significantly by state, with some jurisdictions placing strict limits on these fees or prohibiting them entirely for certain loan types:

- California: Prepayment penalties prohibited on consumer loans under $250,000

- New York: Limited to 2% of amount prepaid, maximum $2,000, only for loans over $250,000

- Illinois: Cannot exceed 2% of original loan amount

- Texas: No state restrictions; governed by federal guidelines and loan terms

- Florida: Limited to 2% of amount prepaid within first 12 months

Borrowers in states with strong consumer protections face lower effective penalty risks, but state law doesn't guarantee penalty-free borrowing—many lenders structure their loans to comply with the most restrictive states while still charging penalties in others.

Red Flags: How to Identify Predatory Penalty Structures

Not all prepayment penalties are created equal. Some are reasonable cost-recovery mechanisms; others are designed to trap borrowers in expensive long-term arrangements. Watch for these warning signs:

The 3-2-1 Structure Trap

Some lenders employ declining penalty schedules (3% in year one, 2% in year two, 1% in year three) that sound consumer-friendly but effectively penalize early payoff throughout most of the loan term. A truly borrower-friendly loan would eliminate penalties after 12 months or waive them entirely.

Percentage of Original vs. Remaining Balance

This distinction matters enormously. A 2% penalty on a $40,000 loan paid off at month 6 with $38,000 remaining costs $760. But if calculated on the original balance, that same loan costs $800—and if the penalty applies to the original balance even as you've paid down principal, you're effectively being charged for money you've already repaid.

Extended Penalty Windows

Standard industry practice limits prepayment penalties to the first 12 to 24 months. A penalty window extending beyond 24 months is aggressive and should prompt serious scrutiny of the lender's motives.

No Grace Period for Rate Changes

Some lenders structure penalties so that if you refinance with them (say, to get a better rate), you still pay the penalty on the old loan. This prevents borrowers from benefiting from their improved creditworthiness—a significant red flag.

The Hidden Cost Connection: BNPL and Alternative Financing

As consumers increasingly turn to alternative financing options for debt management, prepayment penalties aren't the only fees worth understanding. Our research has found that buy-now-pay-later (BNPL) services and point-of-sale financing carry their own complex fee structures that can complicate debt consolidation strategies. For a detailed breakdown, see our investigation into BNPL hidden costs and their impact on consumer credit.

Economic Context: Why Prepayment Penalties Matter More in 2026

The prevalence of prepayment penalties intersects with broader economic pressures facing American consumers. Our analysis of the K-shaped economy's impact on household debt found that lower-income households are more likely to consolidate debt—and more likely to encounter lenders with aggressive penalty structures.

In 2026, median household savings rates remain below pre-2020 levels, meaning fewer consumers have emergency funds to absorb unexpected fees. A $1,200 prepayment penalty can represent two to three weeks of take-home pay for median-income households, making the difference between a manageable payoff timeline and extended debt servitude.

Price-Quotes Research Lab observes that prepayment penalties disproportionately impact the borrowers least equipped to absorb them—a pattern that warrants continued regulatory attention and consumer education.

Strategic Approaches: How to Avoid Prepayment Penalties Legitimately

Consumers aren't helpless against prepayment penalties. Several legitimate strategies can help avoid or minimize these fees:

Strategy 1: Choose Penalty-Free Lenders From the Start

The most direct approach: work with lenders who don't charge prepayment penalties. As documented above, SoFi, Marcus, LightStream, Discover, and most credit unions offer debt consolidation loans without these fees. The tradeoff may be slightly higher interest rates or stricter credit requirements, but for borrowers planning aggressive payoff, the long-term savings typically outweigh those differences.

Strategy 2: Time Your Application to Your Payoff Ability

If you've already saved significant funds for debt payoff, apply for a shorter-term loan. A 24-month consolidation loan with no prepayment penalty may have higher monthly payments but eliminates the window during which penalties would apply—and costs less in total interest than a 60-month loan you'd pay off early.

Strategy 3: Negotiate Penalty Waivers

Many borrowers don't realize prepayment penalty terms are often negotiable, particularly for larger loan amounts or applicants with strong credit profiles. A single phone call asking "what would it take to eliminate the prepayment penalty?" can yield surprising results. Lenders want your business and may trade penalty provisions for slightly higher rates or fee income elsewhere.

Strategy 4: Time Extra Payments Outside Penalty Windows

If you're already in a loan with a prepayment penalty, coordinate extra payments to avoid triggering fees. If your penalty window is 12 months, make regular extra payments starting in month 13. If it's 24 months, wait until month 25 for lump-sum payoffs. The interest savings from even partial early payment typically exceed penalty costs, but timing matters.

Strategy 5: Refinance Into Penalty-Free Products

Once your current loan's penalty window expires, refinance into a penalty-free product. This strategy works best when interest rates have remained stable or declined, and when the refinancing savings exceed any new loan origination fees.

What to Do Next: Your Prepayment-Penalty-Free Consolidation Checklist

If you're considering debt consolidation in 2026, take these steps to minimize or eliminate prepayment penalty exposure:

- Get your current credit profile: Check your credit score and review your credit report. Borrowers with scores above 700 have access to the widest range of penalty-free options.

- Calculate your actual payoff timeline: Be honest about when you can realistically pay off the consolidation loan. If it's under 24 months, prioritize lenders with no penalties or short penalty windows.

- Compare at least three penalty-free lenders: SoFi, Marcus, LightStream, and your primary credit union should be on your comparison list. Get prequalification quotes—these typically involve only soft credit inquiries.

- Read the loan agreement specifically for prepayment terms: Don't rely on marketing materials. Look for "prepayment penalty," "early payoff," or "repayment flexibility" language in the actual loan documents.

- Ask directly about penalty structures: During the application process, ask the lender representative: "If I pay this loan off early or make significant extra payments, will I incur any fees?"

- Factor penalties into your total cost calculation: If a lender offers a lower rate but charges a 2% prepayment penalty, calculate whether the rate savings exceed the potential penalty over your actual payoff timeline.

- Consider balance transfer alternatives: For credit card debt specifically, a 0% APR balance transfer may eliminate interest entirely without prepayment concerns. Compare total costs before deciding.

Frequently Asked Questions

Can a lender charge a prepayment penalty on any type of debt consolidation loan?

Prepayment penalties are generally permitted on unsecured personal loans used for debt consolidation. However, they are prohibited on qualified mortgages under the Dodd-Frank Act, and many states have additional restrictions. Always verify penalty legality in your state and review your specific loan agreement.

How do I find out if my current loan has a prepayment penalty?

Prepayment penalty terms appear in your loan agreement, typically in a section titled "Prepayment," "Early Repayment," or "Repayment Flexibility." If you have the original loan documents, search for these terms. If you don't have copies, contact your lender directly and request the prepayment terms in writing.

Are prepayment penalties tax-deductible?

In some circumstances, yes. If the debt being consolidated includes business expenses, or if the loan is secured (like a home equity consolidation loan), prepayment penalties may be partially deductible. Consult a tax professional for guidance specific to your situation. For personal unsecured consolidation loans, prepayment penalties are typically not deductible.

What's the maximum prepayment penalty a lender can legally charge?

Federal law limits prepayment penalties on certain qualified mortgages to no more than 2% of the original loan amount during the first three years. However, this applies only to loans meeting specific criteria. For non-qualified loans, maximum penalties vary by state. Some states have no limits; others cap penalties at 1-3% of various balance calculations.

Should I avoid lenders with prepayment penalties entirely?

Not necessarily. If a lender with a prepayment penalty offers significantly better rates—say, 2 percentage points lower than penalty-free alternatives—the math may still favor accepting the penalty, particularly if you don't plan to pay off early. Run the numbers for your specific situation before eliminating options based solely on penalty presence.

Conclusion: Protect Your Right to Pay Off Debt on Your Terms

Prepayment penalties represent a fundamental tension in debt consolidation: the very act of aggressively pursuing financial freedom can trigger financial penalties. For Maria Delgado and thousands of borrowers like her, discovering these fees after the fact transforms a strategic financial move into a frustrating setback.

The solution isn't to accept penalties as inevitable—it's to make informed decisions from the outset. By understanding which lenders charge these fees, how they're calculated, and what alternatives exist, consumers can structure debt consolidation strategies that reward their discipline rather than punishing it.

Price-Quotes Research Lab continues to monitor prepayment penalty trends across the debt consolidation industry. As of 2026, the market shows encouraging movement toward penalty-free products, but traditional lenders and certain online platforms continue to embed these costs in loan agreements. Borrowers who do their homework before signing can avoid becoming the next cautionary tale—and keep more of their hard-earned money on the path to debt freedom.