Bankruptcy Filings Surged 18% in Early 2026 — The Exact Costs, Eligibility Rules, and Debts That Survive Each Chapter

Bankruptcy Filings Surged 18% in Early 2026 — The Exact Costs, Eligibility Rules, and Debts That Survive Each Chapter

Published 2026-06-11 • Price-Quotes Research Lab Analysis

The Numbers Behind the Surge

In the first quarter of 2026, bankruptcy filings across the United States climbed 18% compared to the same period in 2025, according to data from the Administrative Office of the U.S. Courts. That's 112,847 new filings in January through March alone — roughly one bankruptcy every 88 seconds. Behind each number is a family that exhausted every other option.

Price-Quotes Research Lab observes that this surge tracks directly with the compounding pressure of medical debt, auto loan defaults, and the lingering K-shaped economic recovery that has widened the gap between households with liquid savings and those living paycheck to paycheck. The median filer in 2026 carries $47,300 in unsecured debt — credit cards, medical bills, personal loans — against a household income that hasn't kept pace with inflation in essential categories like housing and groceries.

This isn't a story about reckless borrowing. It's a story about a system where buy-now-pay-later schemes and medical emergencies can cascade into financial catastrophe faster than most people can react. If you're researching bankruptcy as an option, you deserve specific numbers — not vague estimates. That's what this article delivers.

Chapter 7 vs. Chapter 13: The Fundamental Difference

Before diving into costs and eligibility, you need to understand the two primary bankruptcy pathways for individuals. These aren't interchangeable options — they serve fundamentally different financial situations.

Chapter 7: Liquidation Bankruptcy

Chapter 7 wipes out eligible debts entirely through a court-supervised process where non-exempt assets may be sold to pay creditors. The process typically takes 4-6 months from filing to discharge. In 2026, approximately 67% of personal bankruptcy filings are Chapter 7 cases.

The key advantage: speed and completeness. If you qualify, most unsecured debts disappear within half a year. The key limitation: you must pass a means test, and high-income earners may be redirected to Chapter 13.

Chapter 13: Reorganization Bankruptcy

Chapter 13 creates a 3-5 year repayment plan based on your disposable income. You keep your assets — including your home and car — but pay back a portion of your debts through a court-approved plan before receiving a discharge. In 2026, the average Chapter 13 plan runs 48 months.

The key advantage: asset protection and the ability to catch up on missed mortgage or car payments. The key limitation: it's a longer commitment, and you must have regular income to fund the plan.

Exact Costs for Each Chapter in 2026

Bankruptcy isn't free, and the total cost varies significantly depending on whether you hire an attorney, which chapter you file, and your state's specific requirements. Here's the complete breakdown:

| Cost Category | Chapter 7 (2026) | Chapter 13 (2026) |

|---|---|---|

| Court Filing Fee | $338 | $313 |

| Credit Counseling (pre-filing) | $50-$100 | $50-$100 |

| Financial Management Course (post-filing) | $50-$75 | $50-$75 |

| Attorney Fees (average) | $1,500-$3,500 | $3,000-$6,500 |

| Attorney Fees (complex cases) | $4,000-$6,000 | $6,000-$10,000 |

| Total Typical Cost Range | $1,988-$4,013 | $3,413-$6,988 |

The wide range in attorney fees reflects geographic variation and case complexity. A straightforward Chapter 7 with minimal assets in a rural district might cost $1,200-$1,800 in attorney fees. A Chapter 13 with business debts, multiple properties, or contested issues in a major metropolitan area could run $8,000-$12,000 total.

Critically, you can file bankruptcy without an attorney — this is called filing "pro se." The court filing fee ($338 for Chapter 7) is the only mandatory cost. However, the complexity of means testing, asset exemptions, and creditor negotiations means that pro se filers have significantly higher case dismissal rates. In 2025, 23% of pro se Chapter 7 cases were dismissed compared to 4% of attorney-represented cases, according to the National Bankruptcy Review.

The Means Test: Who Actually Qualifies for Chapter 7

The means test is the gatekeeper for Chapter 7 eligibility. It compares your household income to the median income for your state and household size. If you're below the median, you pass automatically. If you're above, you proceed to a secondary calculation that deducts allowed expenses from your income.

2026 Median Income Thresholds by Household Size

| Household Size | 48 Contiguous States | Alaska | Hawaii |

|---|---|---|---|

| 1 Person | $60,184 | $75,230 | $69,422 |

| 2 People | $79,108 | $98,885 | $91,040 |

| 3 People | $91,456 | $114,320 | $105,294 |

| 4 People | $105,623 | $132,029 | $121,467 |

| Each Additional Person | $9,200 | $11,500 | $10,600 |

These figures are updated annually by the Census Bureau and the Justice Department. For a family of four in Ohio, if your combined household income is under $105,623, you pass the first step of the means test and can file Chapter 7.

If your income exceeds the median, the test calculates whether you have "disposable income" remaining after allowed expenses. The formula deducts secured debt payments (mortgage, car loans), priority expenses (child support, alimony), and standard living expenses based on IRS National Standards. If your disposable income is less than the total debt threshold ($8,025 for most filers, representing roughly 25% of median income), you qualify for Chapter 7.

If your disposable income exceeds the threshold, you're presumed to have abused Chapter 7, and the court may either dismiss your case or convert it to Chapter 13. This doesn't mean you're ineligible for bankruptcy — it means Chapter 7 isn't available to you, but Chapter 13 remains an option.

Debts That Survive Bankruptcy: What Doesn't Get Wiped

This is where many filers get surprised. Bankruptcy eliminates most unsecured debts, but federal law explicitly carves out certain categories. Here's what survives each chapter:

Debts Generally Not Discharged in Either Chapter

- Federal Student Loans: Unless you prove "undue hardship" through a separate adversary proceeding — a standard most courts interpret strictly. In 2025, only 0.4% of student loan borrowers who filed for bankruptcy obtained a full discharge. Private student loans are treated similarly unless they don't meet the "educational benefit" definition.

- Most Tax Debts: Income taxes less than three years old, trust fund taxes, and tax penalties on those taxes. Older income taxes (more than three years old, properly filed) may be dischargeable.

- Child Support and Alimony: Both current and past-due amounts. These are priority debts that survive bankruptcy.

- Criminal Fines and Restitution: Including DUI-related judgments.

- Personal Injury Judgments from DUI: If you were found liable for injuries while intoxicated.

- Homeowners Association Dues: For condos and planned communities, post-petition HOA fees continue to accrue.

Debts That May Survive Chapter 13 But Not Chapter 7

Some debts can be included in a Chapter 13 repayment plan but may not be dischargeable if you don't complete the plan. These include certain tax debts and debts from fraud. The distinction matters: in Chapter 13, you pay what you can through the plan, and remaining amounts may be discharged upon successful completion. In Chapter 7, these debts are simply not discharged.

Secured Debts: A Different Category

Secured debts — mortgages and car loans — aren't eliminated by bankruptcy. You have three options: (1) reaffirm the debt and continue payments, (2) redeem the collateral by paying its current value in a lump sum, or (3) surrender the collateral and the deficiency balance becomes unsecured debt subject to discharge.

For example, if you owe $28,000 on a car worth $18,000, you can reaffirm the $28,000 debt, redeem it for $18,000, or surrender it and owe $10,000 (the deficiency) as unsecured debt. Each option has different long-term implications for your credit and your ability to retain transportation.

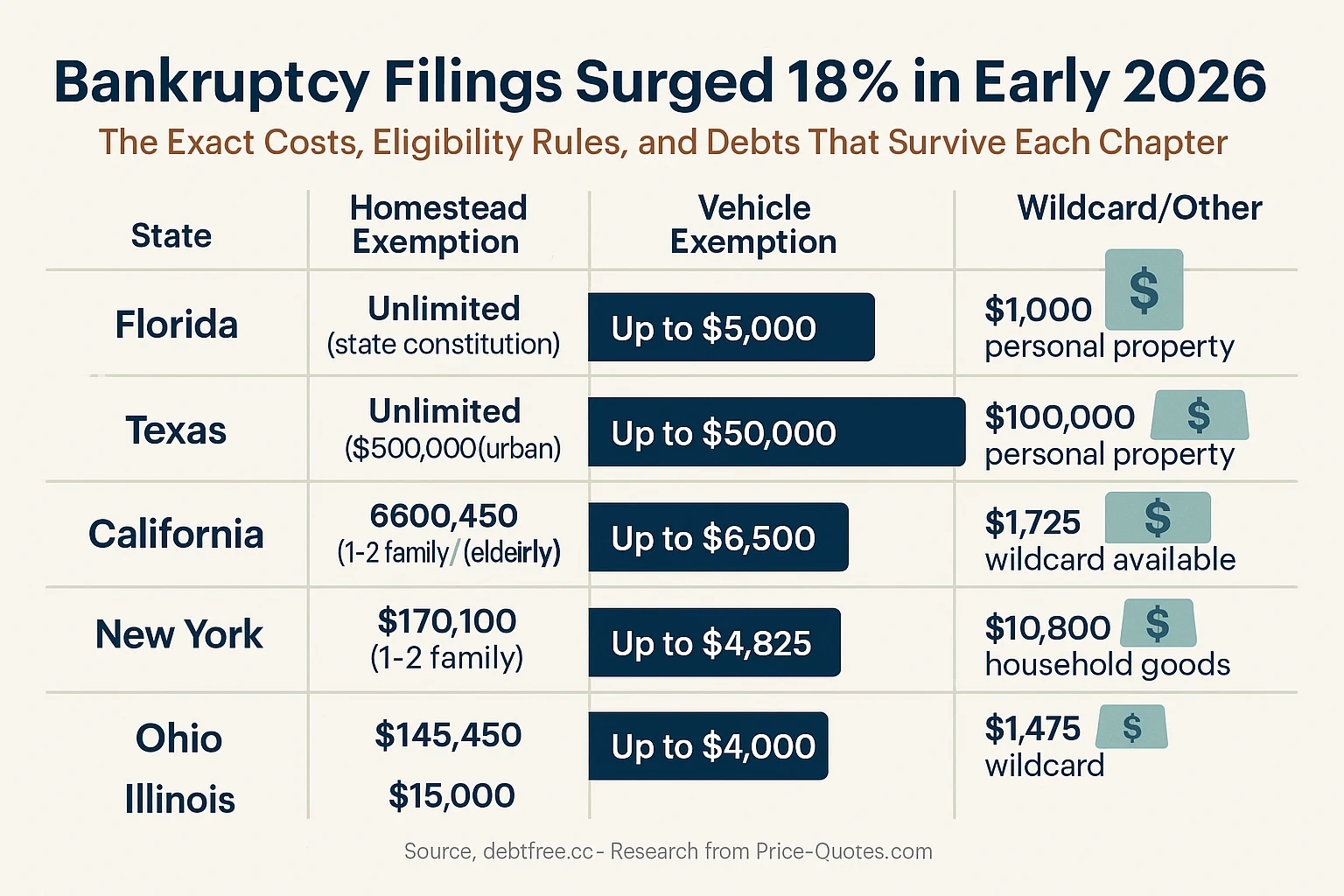

State-by-State Variation: Exemptions That Change Everything

Bankruptcy is federal law, but states control the exemption rules — the assets you're allowed to keep. This creates massive variation in outcomes. In Texas, you can protect unlimited homestead equity. In California, the wildcard exemption allows flexibility but caps home equity at roughly $600,000 for median-priced areas.

Price-Quotes Research Lab observes that this exemption variation explains why identical financial situations can produce dramatically different bankruptcy outcomes depending on where you live. A homeowner with $150,000 in equity might lose their home in New Jersey (limited exemption) but keep it entirely in Florida (unlimited homestead).

Key Exemption Categories by State (2026)

These exemption amounts are adjusted periodically. Before filing, verify current figures with a local bankruptcy attorney or the court's website. Mistakes here can be catastrophic — you might lose assets you thought were protected.

The Hidden Costs of Not Filing

Consumers often delay bankruptcy because of stigma or misinformation. But the math frequently favors filing. Consider the alternative: a household carrying $50,000 in credit card debt at the average 2026 rate of 24.99% APR, making minimum payments of 2% of balance:

- Time to payoff: 21 years and 4 months

- Total interest paid: $68,340

- Total paid: $118,340

Compare that to a Chapter 7 filing costing $2,500 total. The breakeven point comes in under six months of interest payments. For medical debt — which often carries higher rates and fewer hardship options — the calculation is even more stark.

There's also the question of debt collection practices. The CFPB received 261,000 debt collection complaints in 2025, with bankruptcy identified as the only reliable legal mechanism to stop wage garnishment, bank levies, and harassing calls. Creditors continue reporting to credit bureaus during collection, and judgments can attach to property. Bankruptcy triggers an automatic stay that halts all collection activity within 24-48 hours of filing.

What to Do Next: A Decision Framework

If you've read this far, you're likely somewhere in the decision-making process. Here's a practical framework:

Step 1: Calculate Your Total Debt and Income

List every debt: balance, interest rate, minimum payment, and creditor. Calculate your household's gross monthly income from all sources. You need these numbers before anything else.

Step 2: Check Your State's Median Income

Compare your household income to the 2026 median for your state and household size. If you're below the median, Chapter 7 is likely available. If you're above, Chapter 13 may be your path — or you may find that your disposable income calculation still qualifies you for Chapter 7.

Step 3: Inventory Your Assets

Know what you own: home equity, vehicle values, retirement accounts (401k and IRA balances are generally protected in bankruptcy), bank accounts, and valuable personal property. This determines whether you need Chapter 13 to protect assets or whether Chapter 7's speed makes sense.

Step 4: Get a Free Consultation

Bankruptcy attorneys are required to offer free initial consultations. Many offer them by phone or video. Bring your numbers. Ask specifically about attorney fees for your situation, your state's exemption rules, and whether Chapter 7 or 13 fits your circumstances. Avoid attorneys who quote fees without reviewing your specific situation.

Step 5: Consider Credit Counseling

Pre-filing credit counseling is mandatory — but it's also genuinely useful. Approved agencies can help you understand whether alternatives like debt management plans might work. The cost is $50-$100, and the session takes 90 minutes to 2 hours. It's required within 180 days before filing.

The Bottom Line

Bankruptcy in 2026 carries real costs: filing fees of $313-$338, attorney fees ranging from $1,500 to $10,000 depending on complexity, and the time investment of credit counseling and financial management courses. It carries real consequences: a Chapter 7 stays on your credit report for 10 years, a Chapter 13 for 7 years, and you'll face higher insurance premiums and potential employment screening questions.

But for households drowning in $40,000, $60,000, or $100,000+ of unsecured debt, it's often the fastest path to a functional financial life. The 18% surge in filings reflects not moral failure but mathematical reality: at 25% APR, debt compounds faster than most households can pay. Bankruptcy exists precisely because Congress recognized that some situations require a legal reset.

The decision is personal. The numbers should be clear. Armed with the specifics above — actual costs, actual eligibility thresholds, actual debts that survive — you can have a more informed conversation with a bankruptcy attorney and make a decision based on your actual situation rather than general impressions.