DebtFree Research

Teachers face $45,000 more debt than healthcare professionals

Teachers hold $45,000 more education debt than healthcare workers in 2026. We break down the real numbers, ...

Compare top-rated Credit Card Debt Relief professionals in the Tampa area. All providers are licensed, insured, and reviewed by real customers.

Compare Options BelowTeachers hold $45,000 more education debt than healthcare workers in 2026. We break down the real numbers, ...

New 2026 research shows debt payoff success rates soar 40% faster with $1,000 emergency savings. Real data ...

Discover the hidden costs and payment shocks in 2026 debt consolidation loans. Real APR data, origination f...

The 2-point gap between 43% and 41% DTI could cost you a mortgage. Discover the 2026 approval thresholds, r...

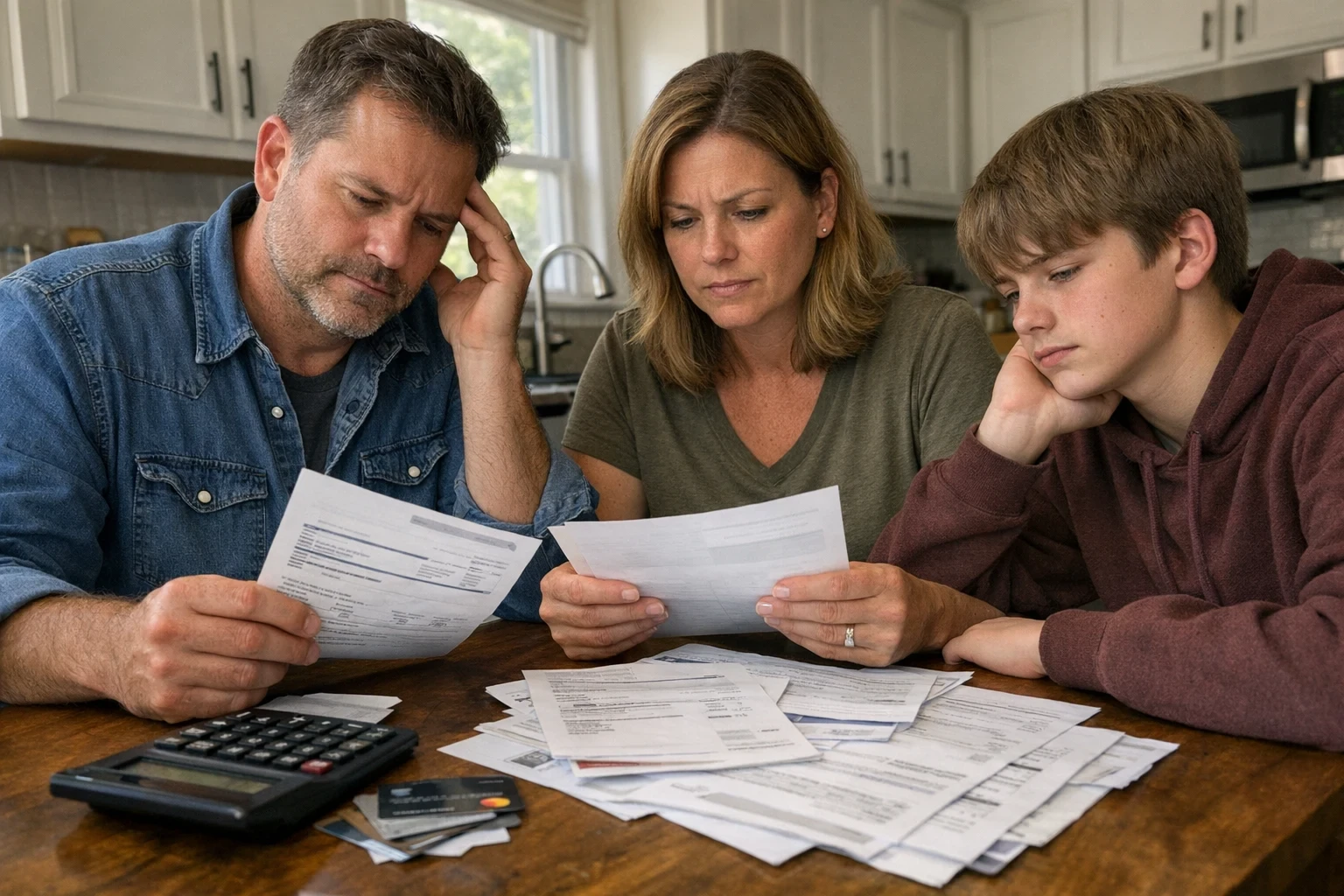

Credit card debt relief includes various strategies aimed at reducing debt. You may need this service if your credit card balances exceed 40% of your total credit limit, or if you’re struggling to make minimum payments. Conversely, if you're still able to pay your bills on time, you might not need these services yet.

Consider credit card debt relief when your monthly payments are causing stress. If you receive calls from collectors or if your credit score has dropped below 600, it’s wise to explore your options. If your debt is manageable, it might be better to handle it without external help.

The process typically starts with a complimentary consultation to assess your financial situation. You'll analyze your debts and income, followed by setting a budget. Then, a debt relief company may negotiate lower interest rates or set up a debt management plan (DMP). This usually involves making a single monthly payment to a third party who pays your creditors. The process can take anywhere from 6 months to several years depending on the amount of debt and the agreements made.

Credit card debt relief can take between 12 months for negotiations and setup. Monthly contributions can last from 3 to 7 years, depending on your total debt and the specific program. Be aware that while you work on relief, your credit score may take a hit initially, but it should improve as you pay off your debts.

The cost for credit card debt relief services can range from $0 to 15% of your total debt. For example, if you have $10,000 in debt, you might pay around $1,500 in fees over the course of the program. Factors affecting costs include the total amount of debt. Certain providers may charge monthly fees ranging from 10 to 100 for ongoing support.

According to Price-Quotes Research Lab data for Tampa, FL, the average cost for Credit Card Debt Relief services ranges based on complexity, time of service, and provider experience. Prices in the Tampa metropolitan area may differ from national averages due to local market conditions, licensing requirements, and seasonal demand. Data reflects verified quotes collected from licensed providers serving Tampa as of July 2026.

Source: Price-Quotes Research Lab, DebtFree Tampa Market Report (2026). Methodology: Aggregated pricing data from verified, licensed providers. Sample covers the Tampa, FL metropolitan area.

| Service | Low | Average | High | Unit | Confidence |

|---|---|---|---|---|---|

| Bankruptcy Filing | $1200 | $1800 | $2500 | per job | ●●●○○ |

| Credit Card Debt Relief | $1500 | $4000 | $7500 | per job | ●●●○○ |

| Credit Counseling | $50 | $75 | $100 | per visit | ●●●○○ |

| Credit Repair | $99 | $199 | $299 | per month | ●●●○○ |

| Debt Consolidation | $500 | $1500 | $3000 | per job | ●●●○○ |

| Debt Settlement | $1500 | $3000 | $6000 | per job | ●●●○○ |

Source: Price-Quotes Research Lab, Tampa Market Report. Based on 6 service categories. Data collected from verified, licensed providers. Methodology | Audit Trail

Price-Quotes Research Lab data shows no price data is currently available for debt services in Tampa. This means the market is still developing, or that data collection is ongoing. The need for these services may vary significantly across Tampa's diverse neighborhoods. For instance, areas like Hyde Park, with their historic homes and potential for high property values, might see a different demand profile than neighborhoods like Seminole Heights, known for its revitalized bungalow-style homes and growing young professional population. The prevalence of 1960s ranch-style homes along Gandy Boulevard could also influence debt service needs, particularly regarding home equity loans and refinancing. Understanding the local housing stock and the financial situations of residents is crucial for predicting demand. Furthermore, the city's permitting process, managed by the City of Tampa's Development Services, can impact related financial activities. The lack of available data means we cannot compare Tampa's debt service costs to other cities or the national average at this time.

Our pricing data currently lacks any seasonal analysis for Tampa debt services. However, it's reasonable to anticipate fluctuations tied to local economic trends and the city's seasonal weather patterns. The months leading up to the Tampa Bay Lightning's playoff season, for example, might see increased demand for debt consolidation to free up cash flow for entertainment and travel. Similarly, the hurricane season, running from June 1st to November 30th, could impact demand for debt services related to property damage and insurance claims, though no data is currently available to confirm this. Watch for potential price adjustments during peak tourist seasons and major local events like the Gasparilla Pirate Festival.

Since no pricing data is available, it's impossible to provide a direct cost comparison for debt services in Tampa. However, the absence of data itself suggests that the market is either nascent or highly competitive. Nationally, debt service costs can vary widely. For example, the cost of a debt consolidation loan might range from $1,000 to $5,000, depending on the loan amount and the lender. Local factors like the area's cost of living, which is generally lower than the national average, could potentially influence service fees. The presence of financial institutions in the downtown area may also affect pricing. The lack of readily available data also makes it difficult to assess the impact of permit fees on related financial activities.

Price-Quotes Research Lab • Anonymous • Helps set better industry standards

How would you rate your most recent Credit Card Debt Relief experience?

What was the biggest issue? (pick one)

How much did you pay? (rough estimate is fine)

Thanks! Here's what others in Tampa reported:

Price-Quotes Research Lab Tampa Consumer Satisfaction Survey • Anonymous • Ongoing

Price-Quotes Research Lab • What should EVERY provider do? • 10 seconds

Which should be MANDATORY for all financial service providers? (pick all that apply)

Great picks! Here's what Tampa consumers agree on:

Price-Quotes Research Lab — "What Consumers Want" Standards Report • Tampa, FL

Price-Quotes Research Lab • Quick trade-offs • Helps providers improve

Would you pay a higher rate/fee if it guaranteed...

Interesting! Here's how Tampa residents feel:

Price-Quotes Research Lab — Consumer Willingness-to-Pay Study • Tampa Metro