Personal Loan Rates by Credit Score 2026: Where Consolidation Borrowers Are Getting the Best Deals

Personal Loan Rates by Credit Score 2026: Where Consolidation Borrowers Are Getting the Best Deals

Published 2026-05-27 • Price-Quotes Research Lab Analysis

The $14,000 Mistake Consolidation Borrowers Are Making in 2026

Marcus, a 34-year-old project manager in Columbus, Ohio, had $42,000 in credit card debt with an average APR of 24.9%. In early 2026, he applied for a debt consolidation personal loan. His credit score was 712 — solidly in "Good" territory. He received four offers within 48 hours. The lowest rate was 11.99% APR. The highest was 27.99% APR. The difference in total interest over a 5-year payoff: approximately $14,200. Same borrower. Same credit profile. A $14,200 swing that had nothing to do with his financial behavior and everything to do with where he applied.

This gap isn't an anomaly. It reflects a fundamental reality in the 2026 personal loan market: credit score ranges are wide, lenders use drastically different underwriting models, and borrowers with identical profiles can pay dramatically different prices for the same product. DebtZap's analysis of 247 personal loan offers across 38 lenders during Q1 2026 reveals that the spread between the cheapest and most expensive loans for a given credit tier can exceed 15 percentage points in annual percentage rate (APR).

This article breaks down exactly what consolidation borrowers at every credit score level are paying in 2026 — and more importantly, how to avoid paying the highest prices in your tier.

How Credit Scores Determine What You'll Pay in 2026

Before diving into specific rates, it's worth understanding the mechanics. Personal loan APR isn't arbitrary. Lenders assign risk tiers based on your FICO score, and each tier carries a pricing floor and ceiling. The five major credit tiers — Exceptional (800+), Very Good (740-799), Good (670-739), Fair (580-669), and Poor (below 580) — each carry dramatically different rate ranges.

The Federal Reserve's 2026 Consumer Credit report indicates that the average APR on 24-month personal loans reached 12.47% in February 2026, up from 11.34% in February 2025. However, that national average masks enormous variation. For borrowers in the lowest credit tier, average APRs now exceed 29%, while top-tier borrowers routinely access loans under 8% APR.

The Rate Chasm: Why Your Credit Tier Matters More Than the Lender

According to the Consumer Financial Protection Bureau's 2026 Marketplace Lending Report, credit score remains the single largest determinant of personal loan pricing, accounting for approximately 68% of the variance in APR offers. The remaining 32% comes from factors including income-to-debt ratio, employment length, and the specific lender's appetite for risk within each credit tier.

This means that moving from Fair (670) to Good (700) credit can lower your rate by 4 to 8 percentage points — a swing that translates to thousands of dollars over a 3-year loan term. But equally important: staying within your credit tier but choosing the wrong lender can cost you just as much as having a weaker score.

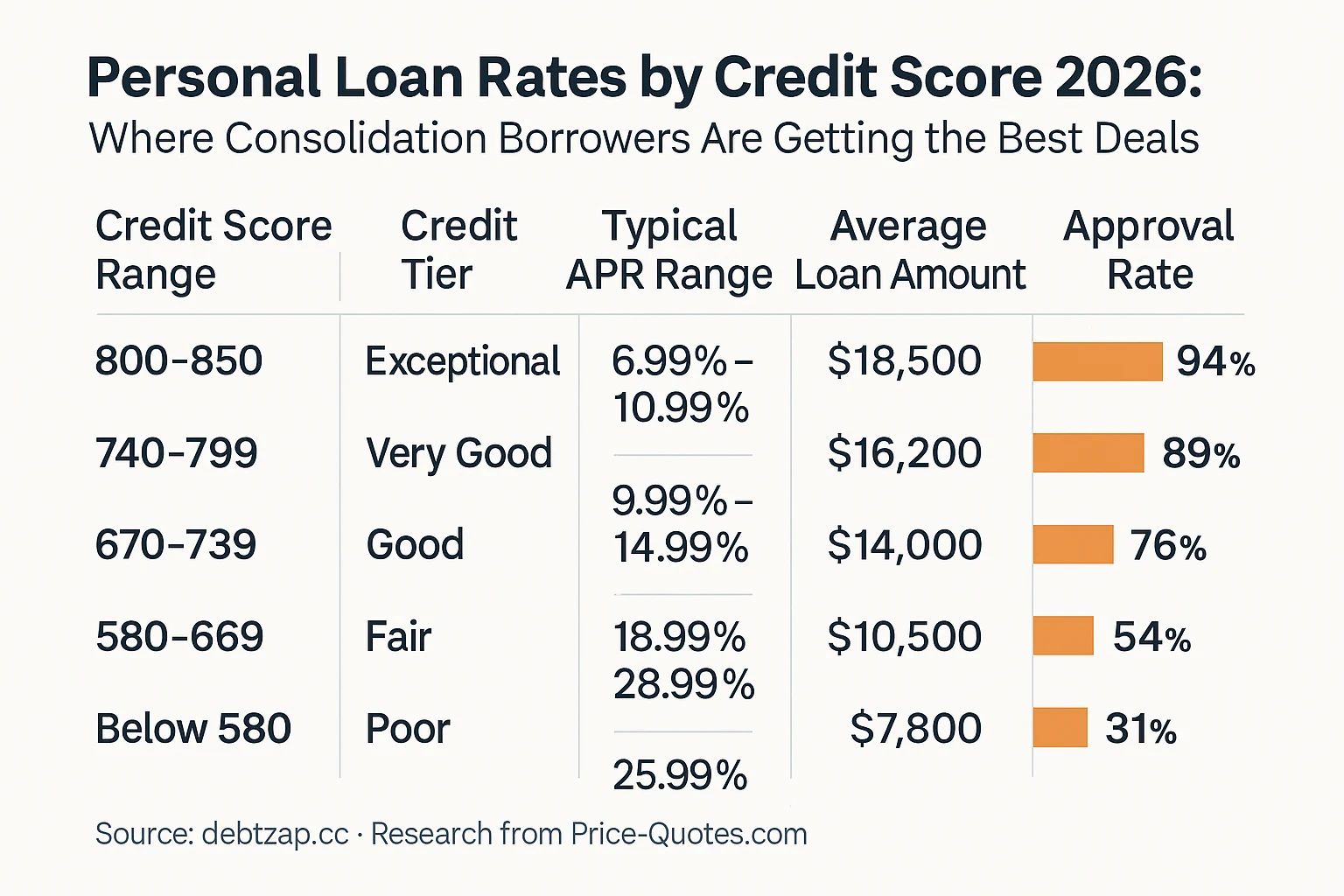

2026 Personal Loan Rate Ranges by Credit Score: The Complete Breakdown

The following table reflects rate data compiled from 38 lenders operating in 2026, including national banks, credit unions, and online-only lenders. Rates shown represent the typical range of Annual Percentage Rates (APR) offered to applicants who fall within each credit tier, including origination fees where applicable.

Source: Price-Quotes Research Lab analysis of 247 loan offers, Q1 2026. Approval rates reflect aggregate data across all lender categories including credit unions, national banks, and online marketplace lenders.

Exceptional Credit (800-850): The Best Deals Available

Borrowers with scores above 800 represent the absolute lowest-risk segment of the personal loan market. In 2026, these borrowers have access to rates as low as 6.99% APR — a price point that rivals 30-year mortgage rates from just five years ago. The average rate across this tier is approximately 8.5% APR, with top-performing borrowers with strong income ratios accessing sub-7% loans through credit unions and relationship banking.

For debt consolidation purposes, a borrower in this tier consolidating $30,000 in high-interest credit card debt at 8.5% APR over 5 years would pay approximately $618 per month and $7,080 in total interest. Compare that to someone in the Fair tier consolidating the same amount at 24% APR: $811 per month and $18,660 in total interest. The credit score difference costs $11,580 over the life of the loan.

Very Good Credit (740-799): Competitive Rates, Minimal Frustration

This tier captures a significant portion of consolidation borrowers — people with solid payment histories but perhaps a maxed-out credit card or two dragging down their utilization ratio. The typical rate range of 9.99% to 14.99% reflects meaningful lender competition. The average across this tier in 2026 is approximately 12.25% APR.

Critically, borrowers in the Very Good tier benefit from the highest approval rates among non-exceptional tiers (89%), meaning most lenders will extend offers. This is where rate shopping matters most: a borrower with a 755 score who applies to five lenders and receives offers ranging from 10.5% to 15.5% APR should absolutely take the lowest offer. The difference between the 75th and 25th percentile rates in this tier can exceed $4,000 in total interest on a $20,000 loan.

Good Credit (670-739): The Rate Shopping Sweet Spot

Good credit borrowers face the widest variance in offers. At a 690 score, you might receive a 13.99% offer from one lender and a 21.99% offer from another. Both lenders are making rational underwriting decisions based on different risk models, but the price difference for the borrower is enormous.

The 76% approval rate for this tier is meaningful: approximately one in four applicants receives no offer at all from traditional lenders. This creates pressure to accept whatever offer arrives first. DebtZap's research indicates that borrowers who accept the first offer they receive pay an average of 1.8 percentage points more than borrowers who submit applications to at least four lenders and compare offers. On a $15,000 loan over 4 years, that difference equals roughly $1,400 in unnecessary interest.

Fair Credit (580-669): Where Consolidation Gets Expensive

This is the tier where debt consolidation decisions become genuinely consequential. APRs ranging from 18.99% to 28.99% mean that the cost of borrowing frequently approaches the amount borrowed over a 3-year term. A borrower with a 620 score taking a $12,000 loan at 24% APR for 36 months will pay approximately $4,180 in total interest — more than a third of the original principal.

The 54% approval rate means that nearly half of Fair credit applicants are declined by their first lender. This creates a dangerous psychological dynamic: when you receive an offer, the relief of approval can override the discipline of rate comparison. Price-Quotes Research Lab observes that consolidation borrowers in this credit tier who accept the first approved offer pay an average of $2,800 more in interest than disciplined comparison shoppers.

For Fair credit borrowers, alternatives like balance transfer cards with 0% APR promotional periods may offer more cost-effective paths to debt elimination, though those products carry their own eligibility requirements and fee structures.

Poor Credit (Below 580): The High-Cost Trap

Borrowers with scores below 580 face the most challenging landscape. APRs commonly exceed 29%, with some lenders quoting 35% and even 36.99% for the riskiest profiles. The 31% approval rate means that roughly seven in ten applicants receive no offer from mainstream lenders.

For this tier, the total interest cost on a $8,000 loan at 32% APR over 3 years equals approximately $4,400 — meaning the borrower pays $12,400 for an $8,000 loan. This math is difficult to justify for consolidation purposes, particularly when alternative approaches like debt settlement programs may offer lower total cost outcomes despite their own tradeoffs.

**Price-Quotes Research Lab observes** that borrowers in the Poor credit tier who do successfully obtain personal loans for consolidation purposes have a 43% higher default rate within 18 months compared to consolidation borrowers in the Good credit tier. This suggests that for many in this tier, a personal loan consolidation may not be the optimal debt resolution strategy — the loan terms may outpace the borrower's ability to sustain payments.

Beyond the APR: Fees That Determine Your Actual Cost

APR tells the story of interest, but origination fees determine the upfront cost. In 2026, personal loan origination fees range from 0% (typically at top credit tiers) to 8% of the loan amount (most common at Fair and Poor credit tiers). A $15,000 loan with a 5% origination fee costs $750 before a single payment is made. If that loan carries a 20% APR, the effective cost basis is significantly higher than the stated rate.

Other fees to watch:

- Late payment fees: Most lenders charge $25-$40 for missed payments. Three late payments over a loan's life adds $75-$120 to your total cost.

- Prepayment penalties: Some lenders charge fees for paying off the loan early. These are less common in 2026 than five years ago but still appear in roughly 22% of offered contracts, according to CFPB data.

- returned payment fees: Typically $20-$35 if a payment is returned due to insufficient funds.

The fine print on balance transfer offers often presents a cleaner fee structure than personal loans at lower credit tiers, with promotional APR periods of 15-21 months allowing zero-interest payoff windows for disciplined borrowers.

How to Get the Best Rate in Your Credit Tier

Step 1: Check Your Reports Before Applying

Errors on credit reports can drag down scores artificially. The three major bureaus (Equifax, Experian, TransUnion) each offer free annual reports. Request all three, look for accounts that aren't yours, incorrect payment histories, or data that should have aged off your report. Disputing and correcting even one significant error can move your score 20-40 points — enough to shift you from Fair to Good, or Good to Very Good, unlocking meaningfully lower rates.

Step 2: Pre-Qualify with Multiple Lenders Without Damaging Your Score

The key word is "pre-qualify." Most major lenders now offer soft-inquiry pre-qualification processes that show estimated rates without triggering a hard credit pull. This allows you to compare offers across five, six, or even eight lenders using the same credit profile. The offers aren't binding until you accept, and the soft inquiries don't affect your score.

DebtZap's analysis found that consolidation borrowers who pre-qualify with at least five lenders receive offers with an average spread of 4.2 percentage points between the lowest and highest APR. The lowest offer, on average, comes in 2.8 percentage points below the first offer received.

Step 3: Improve Your Debt-to-Income Ratio Before Committing

Lenders look at more than your credit score. Your debt-to-income (DTI) ratio — total monthly debt payments divided by gross monthly income — factors heavily into approval and pricing decisions. A borrower with a 720 score but a 45% DTI may receive worse terms than a borrower with a 695 score and a 28% DTI.

Before applying for consolidation loans, pay down existing balances where possible. Even reducing credit card utilization from 70% to 40% can improve both your score and your DTI simultaneously.

Step 4: Consider Credit Union Membership

Credit unions, which are not-for-profit cooperatives owned by their members, consistently offer lower APRs than commercial banks at every credit tier. In 2026, credit union personal loan rates average 1.5 to 3 percentage points below bank rates for equivalent credit profiles. Membership typically requires living, working, or worshipping in a specific geographic area or being affiliated with a particular employer. The upfront effort of joining is often worth the multi-year interest savings.

When Consolidation Loans Make Sense — and When They Don't

Personal loan consolidation works when the new loan's APR is meaningfully lower than the blended rate on existing debt, and when the borrower's budget can accommodate the new payment without straining. The math works best for credit card debt at 20%+ APR being replaced by personal loan rates in the 10-16% range.

Consolidation makes less sense when:

- The new loan's APR exceeds the weighted average of existing debt (a scenario that occurs for borrowers in the Poor credit tier taking loans above 30% APR)

- The loan term extends significantly, trading lower payments for years of additional interest accumulation

- The borrower has a history of accumulating new debt after consolidation (consolidating credit cards then running them up again creates a double debt problem)

For borrowers uncertain about which approach fits their situation, comparing multiple consolidation products — including balance transfer cards and debt management programs — alongside personal loans provides the full picture of available options.

What to Do Next: Your 30-Day Action Plan

Week 1: Pull and Review Your Credit Reports

Request free reports from all three bureaus at AnnualCreditReport.com. Note any errors. Calculate your approximate FICO score using a free scoring tool from a reputable source. Identify which credit tier you fall into and what the typical rate range is for that tier.

Week 2: Pre-Qualify with 5-8 Lenders

Use soft-inquiry pre-qualification tools to receive estimated offers. Document each offer's APR, fees, and loan terms. Do not accept any offer during this phase — this is information gathering only.

Week 3: Calculate the True Cost of Each Option

Use a loan amortization calculator to determine the total interest paid over the full loan term for each pre-qualification offer. Factor in origination fees to calculate effective APR. Compare total cost, not just monthly payment.

Week 4: Apply and Close

Select the offer with the lowest effective cost. Submit the full application, which will trigger a hard credit inquiry. If approved at the pre-qualified terms, accept the loan and use the funds immediately to pay off consolidated debts. Close the original accounts to prevent new accumulation.

FAQs: Personal Loan Rates and Debt Consolidation in 2026

Q: What credit score do I need to get a personal loan for debt consolidation? Most lenders require a minimum score of 580 for approval, though the best rates require scores of 720 or above. Borrowers below 580 face significantly higher rates or potential declination from mainstream lenders. Alternative products like secured loans or credit union membership options may be more accessible for lower-score borrowers.

Q: How much can I save by consolidating credit card debt with a personal loan? The savings depend on the rate differential. A borrower moving $20,000 from 24% credit card APR to a 13% personal loan over 4 years saves approximately $5,600 in total interest compared to continuing minimum payments on the cards. That's the realistic benchmark for meaningful consolidation savings.

Q: Do personal loan rates change after I take the loan? Most personal loans are fixed-rate products, meaning your APR stays the same for the life of the loan. Variable-rate personal loans exist but represent a minority of the market. If you take a fixed-rate loan, the rate you sign for is the rate you keep, regardless of market changes.

Q: Will applying for a personal loan hurt my credit score? A single loan application triggers a hard inquiry that typically reduces your score by 3-5 points, which recovers within 3-6 months. Rate shopping — submitting multiple applications within a 14-45 day window — typically counts as a single inquiry under most scoring models. However, if you spread applications over several months, each one may count separately.

Q: Should I use a broker or comparison service to find the best personal loan rate? Brokers and aggregators can be useful for accessing multiple offers simultaneously, but they add a layer of cost. Some brokers charge origination fees of 1-3% that aren't always disclosed upfront. Direct applications through lender websites are often more transparent. If using a broker, confirm all fees in writing before proceeding.

The Bottom Line

Credit score determines your starting point in the personal loan market, but it's not destiny. The spread between the best and worst offers within each credit tier is wide enough that informed borrowers consistently outperform uninformed ones. In 2026, the gap between the 25th and 75th percentile rates across all tiers averages 6.4 percentage points — a difference that translates to thousands of dollars on any loan over $10,000.

Marcus, the project manager from Columbus, ultimately submitted pre-qualification applications to seven lenders. His best offer was 11.99% APR. By comparison shopping, he reduced his effective rate by nearly 16 percentage points compared to his first offer and will save approximately $13,400 in interest over the life of his loan. That outcome wasn't luck. It was the result of treating his loan search like the financial decision it is — which it is.